Choosing the right health insurance for your family in India isn’t just about premiums or fancy ads. It’s about real protection when things go wrong. And if you’ve ever compared plans online, you already know—it gets confusing fast.

I’ve been there. A couple years ago, I sat with 10+ tabs open, comparing policies for my own family. Same words everywhere—“comprehensive,” “cashless,” “best plan.” But the details? Totally different. And honestly, I almost picked the wrong one because I ignored the fine print.

So this guide is built to help you compare health insurance for family India properly, without fluff, without marketing noise.

What Is Family Health Insurance (Family Floater Plan)?

A family floater health insurance plan covers multiple family members under a single sum insured.

Instead of buying separate policies, you get one shared coverage pool. For example:

- ₹10 lakh sum insured

- Covers: You + spouse + kids

- Anyone can use the full amount if needed

This makes it cost-effective and easier to manage.

Why You Need Family Health Insurance in India

Healthcare costs in India have risen steadily. Even a short hospital stay can burn through savings.

According to guidelines and public information from the Insurance Regulatory and Development Authority of India (IRDAI), having adequate coverage is essential for financial protection against medical emergencies.

Real-life reality:

- Hospital bills are unpredictable

- Lifestyle diseases are increasing

- Medical inflation is real (you feel it, even if no one quotes numbers)

I once saw a friend pay nearly ₹3 lakh for a 3-day hospitalization. No ICU, nothing extreme. That’s when it hits—you don’t want to “figure it out later.”

Types of Family Health Insurance Plans

Before comparing, understand what’s available.

1. Family Floater Plans

Most popular option. One policy covers everyone.

2. Individual + Family Combo

Separate cover for each member + floater backup.

3. Top-Up and Super Top-Up Plans

Extra coverage beyond a certain deductible. Useful if you already have a base plan.

Key Factors to Compare (This Is Where Most People Go Wrong)

Let’s break down the real comparison points. Not just premium.

🔹 1. Sum Insured (Coverage Amount)

Don’t underinsure.

For a metro city, ₹10–20 lakh is a reasonable starting point for a family of 3–4.

For smaller cities, ₹5–10 lakh might work—but rising costs mean higher is safer.

🔹 2. Premium vs Value

Cheapest is not best.

Look at:

- What’s covered

- What’s excluded

- Room rent limits

- Co-payment clauses

Sometimes a slightly higher premium saves lakhs later.

🔹 3. Network Hospitals & Cashless Facility

Cashless treatment matters more than you think.

Check:

- Nearby hospitals in network

- Quality of hospitals, not just quantity

Because in emergency, you won’t be browsing hospital lists.

🔹 4. Waiting Periods

Most policies have waiting periods for:

- Pre-existing diseases (2–4 years typically)

- Specific illnesses

This is why you should buy early. Not when illness already starts.

🔹 5. Room Rent Limits

This is a hidden trap.

If your plan allows only ₹3,000/day room rent but hospital charges ₹6,000—you pay the difference. And not just room… entire bill gets proportionally reduced.

Yes, it’s frustrating.

🔹 6. Co-Payment Clause

Some policies require you to pay a percentage of the bill (like 10–20%).

Avoid if possible, unless premium savings are significant.

🔹 7. Claim Settlement Ratio

Check insurer reliability.

While IRDAI publishes annual reports, you should focus on:

- Claim settlement ratio

- Claim process experience (reviews matter here)

🔹 8. No Claim Bonus (NCB)

If you don’t claim, your sum insured increases.

Example:

₹10 lakh → ₹15 lakh → ₹20 lakh over years

This is a big long-term benefit.

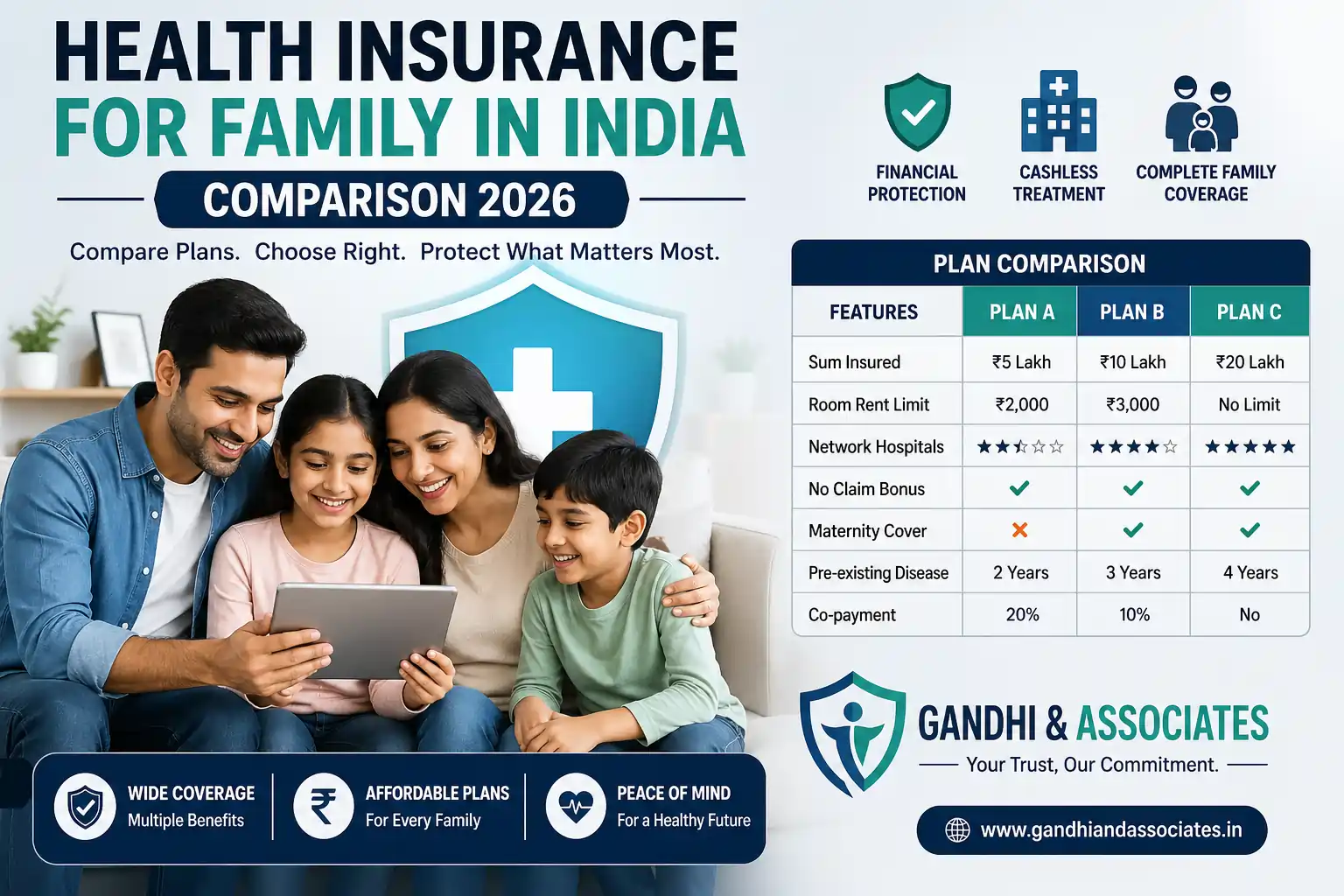

Popular Health Insurance Plans in India (Comparison Snapshot)

Instead of pushing “best” plans (because it depends on your needs), here’s a general comparison approach:

| Feature | Plan A | Plan B | Plan C |

|---|---|---|---|

| Premium | Low | Medium | High |

| Coverage | Basic | Balanced | Comprehensive |

| Room Rent | Limited | No Limit | No Limit |

| Add-ons | Few | Moderate | Extensive |

| Best For | Budget users | Families | Premium coverage |

Always compare on insurer websites or IRDAI-approved platforms.

Common Mistakes People Make (I Almost Did Too)

❌ Buying Only Based on Premium

Looks cheap now, expensive later.

❌ Ignoring Fine Print

Especially exclusions and limits.

❌ Delaying Purchase

Waiting period becomes a problem later.

❌ Not Disclosing Medical History

This can lead to claim rejection. Be honest, always.

Tax Benefits You Should Know

Under Section 80D of the Income Tax Act:

- Up to ₹25,000 deduction (for self & family)

- ₹50,000 if covering senior citizen parents

This makes health insurance even more valuable.

How to Choose the Right Plan for Your Family

Here’s a simple approach:

Step 1: Define Coverage Need

Family size + city + lifestyle

Step 2: Shortlist 3–4 Plans

Don’t compare 20. It gets messy.

Step 3: Read Policy Wordings

Yes, actually read them. Few people do.

Step 4: Check Hospital Network

Near your home, not just big cities.

Step 5: Add Riders if Needed

- Critical illness cover

- Maternity benefits

- OPD cover

My Personal Experience (Honest One)

When I bought my first family plan, I went for a cheaper option.

Looked perfect on paper.

But later I realized:

- Room rent was capped

- Few hospitals nearby were covered

- Claim process was… not smooth

Eventually, I switched plans (after waiting period again, which was annoying).

Lesson learned:

Don’t rush. Compare properly.

Why Comparing Plans Online Isn’t Enough

Most comparison websites:

- Show limited data

- Highlight sponsored plans

- Skip fine details

You need a mix of:

- Official insurer info

- IRDAI guidelines

- Real user experience

How We Help at Gandhi & Associates

If you’re unsure where to start, you can explore https://gandhiandassociates.in/.

We focus on:

- Simplifying complex insurance decisions

- Helping you compare plans honestly

- Avoiding costly mistakes

Not every plan suits every family. That’s the truth.

Read For Informations

- “Best Personal Loan in India Online (2026 Guide)”

- “Best Term Insurance Plan India 2026”

- “Instant Loan App Without CIBIL Check India (2026)”

- “Income Tax Filing Online India”.

Final Thoughts

Health insurance for family in India isn’t just a financial product—it’s peace of mind.

And comparing plans properly is the difference between:

- Being protected

- Or being surprised during a crisis

If you take one thing from this guide, let it be this:

Don’t choose the cheapest plan. Choose the one that won’t fail you when you need it most.

FAQs

1. What is the best family health insurance in India?

There’s no single best. It depends on your needs, budget, and city.

2. How much coverage is enough?

₹10–20 lakh is a good starting point for most families.

3. Can I include parents in family floater?

Yes, but premium increases. Sometimes separate plans work better.

4. Is cashless treatment available everywhere?

Only in network hospitals.

If you’re planning to buy a policy soon, take your time. Compare smartly. And yeah… read the fine print (even if it’s boring). It matters more than you think.

Comments